The significance of crypto taxation has increased with the increasing monitoring of the government on crypto-related trades such as Bitcoin, stablecoins, NFTs, and others.

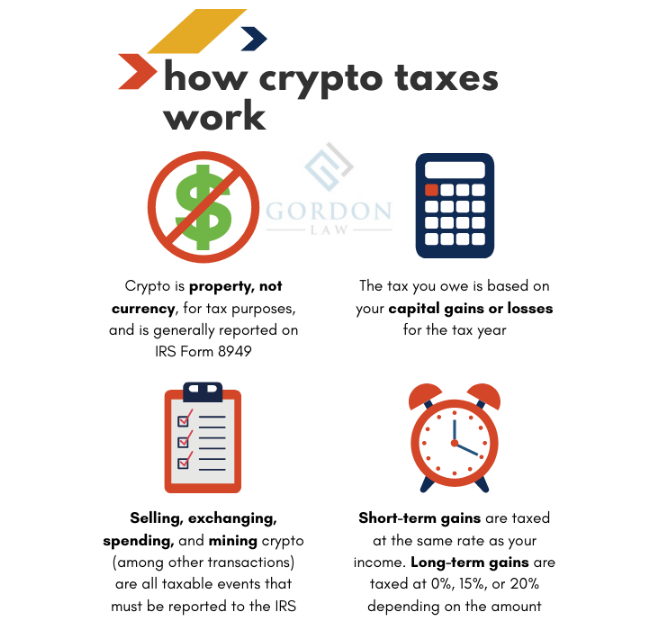

Various regulatory bodies require investors, traders, miners, and even businesses to report on their tax liabilities for any cryptocurrency transactions, as well as calculate profits or losses, or even income, derived from their cryptocurrency holdings. Even though cryptocurrency taxes vary by jurisdiction, cryptocurrencies are generally treated as capital assets rather than regular currency.

Moreover, any transaction regarding the selling, trading, spending, mining, and earning of cryptocurrencies may become taxable. Reporting a taxable transaction, calculating gains and losses, and keeping the relevant documentation can be viewed as some of the major obligations in this regard.

Source: Lexology

Taxable Events and Cryptocurrency Taxes

A taxable event is an activity or a situation where income, gains, losses, and other similar amounts need to be reported to the tax authorities. Buying cryptocurrencies with fiat currency does not qualify as a taxable event in some tax jurisdictions. On the other hand, disposing of the digital currency qualifies as a taxable event.

Taxable events are illustrated below:

- Conversion of digital currency to fiat currency.

- Exchange of one type of digital currency for another.

- Purchase of items using digital currency.

- Mining of digital currency.

- Receiving staking rewards.

- Digital currencies acquired via forks/airdrops.

- Payment of salaries in digital currencies.

The basis of whether a person made a capital gain or a capital loss would lie in the disparity between the cost of the asset and its value at the time it is disposed of.

Common Cryptocurrency Operations and Their Taxation

| Operation | Typical Taxation Approach |

| Purchase of cryptocurrency using fiat | Normally not taxable |

| Sale of cryptocurrency using fiat | Normally taxable |

| Trade of one cryptocurrency for another | Normally taxable |

| Use of cryptocurrency | May cause a gain or loss |

| Miner rewards | Normally taxable |

| Staking rewards | Normally not taxable |

| Transfer from one crypto wallet to another | Normally not taxable |

| Donation to qualifying charities | Normally not taxable |

Tax Calculation on Cryptocurrencies

Calculating cryptocurrency tax mainly revolves around capital gains tax calculation. In most cases, the taxpayer will subtract the investment’s original cost from its current fair market value.

The formula can be illustrated below:

Fair Market Value – Cost Basis = Capital Gain/Capital Loss

In a case where the taxpayer buys two Bitcoins, each valued at $10,000, and sells them at a value of $30,000, the calculation is:

| Calculation Component | Value |

| Purchase Cost | $20,000 |

| Sales Price | $60,000 |

| Capital Gain | $40,000 |

In some cases, the length of time that you have owned something could influence your tax rate.

Taxation of Cryptocurrencies and Income Taxation

Not all cryptocurrency taxes are necessarily capital gains taxes. Certain transactions could earn you taxable income and require you to report such income.

Sources of income in this case would include:

- Mining of cryptos.

- Staking rewards.

- Airdrops.

- Referral bonuses.

- Salary payment or payment for services rendered in cryptocurrency form.

The basis of the tax, therefore, would typically be the market value of the digital asset on its date of acquisition. Any gain or loss would then be recognized when the digital asset is eventually sold.

Record Keeping Requirements

Good record-keeping is essential for tax purposes. As a rule, one would expect the taxpayer to have proper records for the purpose of establishing his/her income and losses.

These include:

- Purchase date.

- Date of sale.

- Value of the asset at time of purchase or sale.

- Transaction fees.

- Exchange documentation.

- Wallet transaction documentation.

- Cost basis documentation.

Such information is necessary to calculate taxes and to confirm reported transactions when tax authorities require it.

Methods Employed for Asset Disposals Calculations

Calculating taxes becomes difficult when investors trade frequently and purchase many of the same assets at varying prices.

The two popular accounting methods are as follows:

FIFO Method (First-In, First-Out)

FIFO means that older assets are disposed of before newer assets. It is the preferred method when no alternative identification system is available.

Specific Identification

Under Specific Identification, taxpayers can identify the exact units sold, provided they keep proper records. Use of the method of Specific Identification could influence the computation of gains or losses because of variation in purchase costs of each unit.

Regulatory Reporting Moves Forward

New regulations require cryptocurrency holders to submit more information to tax authorities. Not only does the new regulatory regime cover individuals, but also exchanges and other service providers.

Regulatory authorities continue to enhance regulatory requirements as the use of cryptocurrencies increases.

Cryptocurrency Taxes Implications for Investors

Cryptocurrency taxes involve numerous transactions, such as sales, trades, use, mining, staking, and receipt of cryptocurrency earnings.

It all depends on the type of activity involved and the basis of the asset in question, among other factors, to determine whether any taxes are due and how much. Since reporting rules are still evolving, it is crucial to have transaction records.

Conclusion

Cryptocurrency taxes continue to be a significant consideration for individuals who deal with buying, selling, trading, mining, staking, or earning cryptocurrency. Regardless of the differences that may exist in tax laws across different locations, there is a common trend whereby most of the jurisdictions treat digital assets as taxable properties, which would mean that any gain, loss, or income from these operations should be taxed.

FAQs

What are cryptocurrency taxes?

Cryptocurrency taxes are taxes paid on either the gain or loss, as well as any income generated through the use of cryptocurrencies. They can be capital gain taxes when selling digital currency, or taxes paid for mining, staking, or generating income using the digital currencies.

Is buying cryptocurrency taxable?

In most cases, the purchase of cryptocurrency for fiat currency is generally not taxable, except when the individual goes to sell or trade their purchased cryptocurrency.

Are crypto-to-crypto trades taxable?

Cryptocurrency trades between two different digital assets are usually considered taxable actions since they will often produce gains or losses within the asset.