The popularity of cryptocurrencies has led to more financial services beyond simple transactions and investments in these assets. Over time, firms have begun offering services that help individuals make money from their cryptocurrencies, lend their cryptocurrencies without actually selling them, and manage their digital currencies through platforms similar to traditional banking services. One such product offered by many firms is known as centralized finance (CeFi)

Through this concept, individuals can use their cryptocurrency to earn interest and receive crypto-backed loans and other financial services provided by a third party.

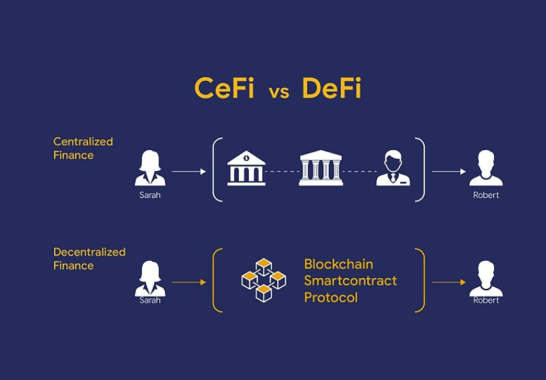

Unlike Decentralized Finance (DeFi), where individuals have full control of their money using smart contracts, CeFi involves the presence of a central entity that is responsible for ensuring the safety of customers’ money as well as taking care of the financial activities of the customer. This has led to the emergence of crypto lending and savings programs.

Source: Binance

What Is CeFi Crypto Banking?

A CeFi crypto banking system is a financial network developed around crypto asset custody. In this system, the user entrusts his funds to a third party, which holds them and offers financial instruments such as interest-bearing accounts and secured loans.

There are similarities between CeFi banking and traditional finance. For instance, in both cases, the customers have to make deposits, monitor their accounts via online applications, and rely on intermediaries for all transactions and security concerns.

However, there are notable differences as well. As opposed to traditional banks, cryptocurrency holdings of CeFi companies are often not covered by government deposit insurance.

Core Features of CeFi

- Custodial storage of customer funds

- Cryptocurrency savings accounts that earn interest

- Cryptocurrency loaning options

- Account management using digital technology

- Verification procedures for identity

- Systems for customer support

Comparison Between CeFi and DeFi

The difference between CeFi and DeFi lies mainly in custody and control.

| Feature | CeFi | DeFi |

| Asset Custody | Maintained by the platform itself | Controlled by the user |

| Functioning | Operated by the central body | Smart contracts execute processes |

| Interaction | Traditional banking experience | Blockchain interactions |

| Risks | Platform and custodial risks | Smart contracts and protocols risks |

| Products | Savings and loans | Liquidity management and earning yields |

However, while both types of services offer ways to make profits from digital assets, they work in completely different ways, with different risks involved.

How the Interest is Produced

In most cases, earning interest on deposited cryptocurrency is a key feature of CeFi banks.

The interest is not calculated by the national banking system but rather depends on market demand for borrowed cryptocurrency. The platform lends the deposited funds to borrowers and pays a portion of the profits to depositors.

The stablecoin usually offers higher interest rates because it is actively used for lending and trading. Sometimes platforms offer other ways to earn money through rewards in the form of tokens.

The value of these tokens can also vary based on the deposited assets, and hence, it presents another risk for users.

Understanding Crypto-Backed Loans

The second important part of CeFi crypto banking is crypto-backed loans.

Contrary to conventional loans, which require a credit check and income confirmation, among other things, crypto-backed loans involve the use of digital currencies to offer guarantees.

The process requires a user to provide collateral in terms of cryptocurrencies and get loans based on their value.

The ratio of the collateral value to the loan amount is called the loan-to-value ratio, LTV.

Elements of a Crypto-Collateralized Loan

| Element | Value |

| Value of Bitcoin Collateral | $48,000 |

| Loan Size | $28,000 |

| LTV | 58% |

| Form of Collateral | Bitcoin |

| Currency Borrowed | Fiat or Stablecoin |

Due to the volatile nature of cryptocurrencies, lenders have minimum standards for protection.

Margin Calls and Risk of Liquidation

Collateral management is one of the critical components of crypto loans.

In case the value of the deposited collateral drops suddenly, the lender can request a margin call. Not meeting those conditions will lead to liquidation, during which some of the collateral will be sold to maintain the required LTV ratio.

The reason is that once collateral has been provided, the platform assumes responsibility for managing the lending risk.

For the borrower, volatility remains one of the major factors to consider when dealing with cryptocurrency loans, as falling asset prices may prompt the sale of collateral despite their plans.

Security Concerns in CeFi

Security is an essential element of CeFi crypto banking.

Since the funds will be entrusted to a third-party service, security measures that will be put in place on the website become very critical in protecting the user’s funds. As opposed to traditional banks, the government does not have an insurance policy that protects against such risks.

Therefore, users typically consider factors such as account custody, account security, reserve management, and transparency when choosing a crypto banking service provider.

Popular Security Measures

- Two-factor authentication

- Biometric authentication

- Address verification

- Identification verification

- Account monitoring

Conclusion

CeFi crypto banking consists of integrating traditional financial services into crypto investments by way of earning interest on assets and obtaining loans using them through a central institution. It contrasts with decentralized finance because users delegate the management of their crypto to a custodial provider in order to be able to make use of financial services.

FAQs

What is CeFi crypto banking?

Cryptocurrency banking under CeFi refers to the process where one can store their crypto to generate profits in the form of interest or take a loan.

How does CeFi differ from DeFi?

In CeFi, you will entrust your funds to the firm while in DeFi, your funds are not required to be entrusted since smart contracts are used.

What is a crypto-back loan?

This is where an individual gets fiat currency or a stablecoin in exchange for their crypto.

What is a margin call in crypto lending?

In this case, the lender finds that the collateral deposited by the client is inadequate and requests more deposits.

Are CeFi deposits insured?

The deposits are usually not covered by government insurance like the conventional bank accounts.