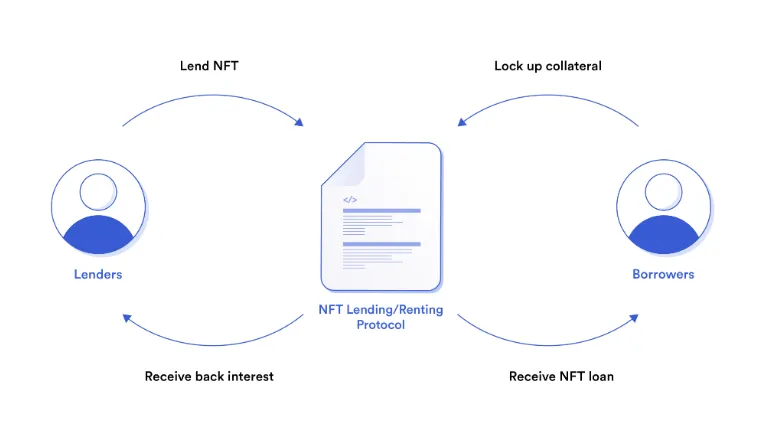

NFT tokens are introducing new possibilities by which owners can access liquidity through means other than selling off their investments. This can be achieved through NFT lending, whereby the owners of the collectibles lend out their tokens as collateral and receive a crypto loan from decentralized finance platforms.

This process involves the use of smart contracts that automatically lock up the user’s digital assets until the repayment of the loan. When the borrower pays off the loan, the NFT is released automatically following the terms of the contract.

NFT lending has been rising due to advancements in the DeFi space. Such platforms allow individuals to submit loan applications, set lending parameters, and provide liquidity for collections with secondary markets.

Source: Chainlink

Such a lending framework has enabled activities in the digital art and collectible world beyond just trading.

How Does NFT Loaning Work Within the Cryptocurrency Industry?

NFT loans do not have much of a difference with conventional lending processes in the decentralized finance world because they also require collateral in order to be able to borrow money. The initial step involved in this type of borrowing is simply depositing the NFT asset into the NFT-friendly lending protocol.

The borrowing process starts with the valuation of the collateral. Once the valuation is done, the borrower receives the loan funds via stablecoin, and the NFT itself stays locked inside the smart contract.

Should the borrower repay the loan during the stipulated time period, the NFT is automatically returned. However, if the terms of repayment are not fulfilled, then the NFT will be automatically liquidated in favor of the lender.

Currently, there are multiple lending platforms for NFTs, such as NFTfi, Blend, Arcade, and BendDAO. Such protocols offer diverse types of NFTs and differ in their lending strategies, which can include both P2P negotiations and pool-based loans.

Valuation and Metrics Are Crucial for NFT Loans

To lend money, platforms have to calculate multiple risk metrics.

For example, if you lend 50 DAI on an NFT with a value of 100 DAI, then your LTV will be 50%. The reason why lending platforms keep LTV at a lower level is that NFT values are unpredictable.

The other important ratio is the liquidation ratio. The ratio defines when the NFT can be liquidated based on whether the value of the asset is lower or whether the borrower is not complying. It is common for some NFT lending platforms to collect liquidation fees together with the rights of ownership.

Another important concept that is considered when taking loans in NFTs is the floor price. Floor price refers to the lowest price at which the NFT can be sold in a collection and is also used to estimate the value of collateral.

Popular NFT collections used in collateralized lending include Bored Ape Yacht Club, CryptoPunks, Azuki, and Pudgy Penguins because they maintain active marketplaces and publicly visible price histories.

| Feature | NFT Loans | Traditional Crypto Loans |

| Collateral Type | NFTs | BTC ETH Stablecoins |

| Valuation Method | Collection floor prices | Market price feeds |

| Liquidity | Lower | Higher |

| Volatility Risk | Higher | Moderate |

| Loan Structures | Peer-to-peer and pooled | Mostly pooled |

| LTV Ratios | Usually lower | Usually higher |

NFT Lending Introduces New Risks to DeFi

NFT loans continue to face several operational and financial risks. NFTs are extremely volatile, particularly during market slumps. Due to the lower liquidity of NFTs relative to crypto coins, there may be difficulties for the lender in disposing of the NFT collateral.

The other possible risk associated with NFT lending involves smart contract risks. Lending NFTs requires automatic actions made possible through smart contracts, including loan repayment and liquidation.

There are also some regulatory uncertainties regarding NFT lending. The authorities of different states are trying to establish whether any particular activity in relation to NFT falls under the scope of the existing regulation.

Nevertheless, NFT loans do not involve any credit checks, as all transactions in the lending process depend solely on the collateralization of digital assets.

NFT Loans Keep Growing in Digital Asset Lending Markets

The market for NFT loans has been adding value to blockchain-based collectibles by providing liquidity for users seeking exposure to digital asset markets. The NFT loan market has also added new dimensions to DeFi related to digital art, games, and collectibles.

NFT-backed P2B Loan Protocol, Source: mapleblock

NFT-backed P2B Loan Protocol, Source: mapleblock

With the reduced liquidity associated with NFTs when compared to cryptocurrencies, there could be difficulties with the sale of these assets used as collateral in a loan.

Companies specializing in industry data, like DappRadar and CoinGecko Research, are continuously monitoring lending activities involving NFTs as the lending industry continues to evolve within decentralized finance infrastructure.

Conclusion

The use of NFT loans has helped incorporate decentralized finance activities into digital collectibles, giving the holders access to liquidity using collateral systems within the blockchain environment. The system involves the use of smart contracts, NFT valuation framework, and liquidation methods.

FAGs

What are NFT loans?

These are crypto-based loans in which the borrower receives liquidity from lenders, using NFTs as collateral.

How does an NFT loan work?

To take out a loan using the NFT assets, the borrower is supposed to lock them up in the borrowing platform that evaluates them to allocate funds as per the agreed upon arrangement.

What happens in case there is no repayment of NFT loans?

In the event that the borrower fails to repay the loan, then the lender has the right to seize their assets through the smart contract arrangement.